Welcoming the Future of Finance with Blockchain

If you have not been living under a rock for the past 12 years, you must have heard about cryptocurrencies like Bitcoin. What you may have missed is the technology behind these, which is called blockchain, is not limited to creating currencies alone. In fact, it has the potential to entirely remodel every industry out there, including the financial institutions.

All the financial institutions right now run on manual networks which are highly prone to theft, errors, and corruptions. Simply replacing the current system with blockchain can resolve all the issues. Many big organizations have already started to realize that and initiated the process of welcoming a more blockchain-enabled future for the finance industry. According to the Global Fintech Report 2017, 77% of Fintech institutes expect to adopt blockchain as part of an in the production system or process by 2020.

What is blockchain?

If we explain in very simple terms, “blockchain” is merely a series of time-stamped “blocks” containing digital information, stored in a public database using cryptographic principles or “chain”. This digital information consists of 3 parts - information about a transaction, information about the participant of that transaction, and special information (hash) which distinguishes every single block from one another.

Why blockchain?

Blockchain is a revolutionary technology that beats every other transaction technology that we have so far because of its very special features

Decentralized network:

The record of data in a blockchain is managed by a cluster of computers instead of one, all run independently, acting on a peer-to-peer basis. It has no central authority controlling it and hence, this data is decentralized.

Distributed ledger:

A “block”, before being added to the “chain”, is verified by potentially millions of computers distributed around the network. So for any transaction to be added to the blockchain, it needs to go through a whole lot of validation process, which makes it more trustworthy than the regular transactions.

Cryptographic Security:

Each user with access to a blockchain is issued two cryptographic keys — private and public. The public key is exposed to all users for verifying request details and other work. However, the identity of the user is hidden with a unique obfuscation called “digital signatures”, which is the private key for the users. This private key is only available to the owner of the data and he/she can unlock it with the encryption created initially at the time of adding the details to the blockchain. This cryptographic security of user access makes it almost impossible for identities to be hacked and data to be compromised.

Data provenance:

The ownership of a digital asset registered on a blockchain can only be modified by the owner itself, unlike on the traditional distributed database management system where the administrator of the system has full control. Therefore, the origins of the assets are traceable and therefore, are verifiable and reusable.

Immutability and transparency:

Each node point in a blockchain has a copy of the entire history of all transactions, hence all data exist simultaneously in multiple places in the network. This reduces the chances of data being lost.

Also, blockchain only supports “create” and “read” functions, which means if data in one block changes, data in all the subsequent blocks change and notifies the whole network. This feature practically makes the data immutable and thus extremely secure.

An extremely important application of blockchain in Australia: Smart contracts

One of the most important applications of blockchain technology is smart contracts. A smart contract is practically the digital equivalent of legal contracts. It is a self-enforcing software managed by a p2p network of computers that facilitate, verify, or enforce the negotiation or performance of a contract.

When a blockchain-enabled smart contract is used, transactions between the nodes are only triggered when all the conditions are met and this is verified digitally by a cluster of independent computers with no human help. Since blockchain is decentralized, it cuts off the intermediary which reduces the possibility of corruption and human error, along with making the entire procedure much faster, cheaper, and more secure than regular contracts. This can be used in all the fundamental functions of a bank such as lending, deposits, treasury, investment advice, business intelligence, regulatory compliance, payments, and remittances.

Blockchain in finance can completely transform the sector

Even though the world has gone digital, the current financial institutions still are highly dependent on paper-based outdated technologies. Moreover, too many intermediaries in every transaction process not only consume a lot of time but make the overall transaction cost go high.

The technology of the future is blockchain and it has the power to shake up the world of finance and make it much better. Let us see how:

Payments across country borders:

Payments across country borders are too expensive and time-consuming at present because of all the collaboration required with corresponding banks and other intermediaries. Blockchain in Australia essentially removes all the intermediaries, so the process of cross border payments becomes much simpler, much less costly, and much faster.

A reduction in corruption:

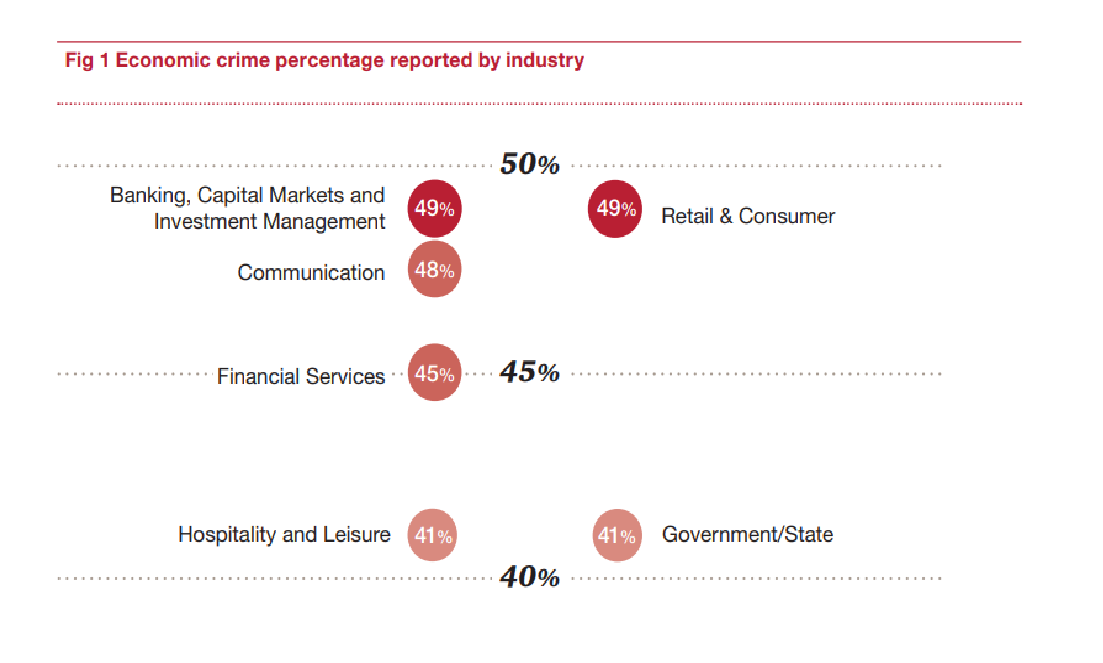

A centralized database system is vulnerable and highly prone to cyber attacks as a single point of failure in such systems can be exploited by hackers to steal money, or at least valuable information. According to a PwC report, 45% of Financial Services organizations have suffered economic crime in its many guises, from fraud and cybercrime to money laundering and bribery and corruption.

Because of the various features of the technology, incorporating blockchain in finance can reduce frauds with its secure record-keeping and transaction methodology, and smart contracts.

- Blockchain is resilient against hacking, DDOS attacks, and other forms of fraud since there is no such single point of failure in the blockchain.

- It can also help banks and others identify individuals quickly and accurately through a blockchain-enabled digital ID.

- Superfast cross-industry data sharing will prevent fraud in insurance claims.

- A blockchain ledger records every data in the supply chain in real-time so that scamming opportunities are much less.

- Stock trading:

Share trading involves many third parties making the process lengthy, such as brokers, CCPs, CSDs and exchanges, all of which will be eliminated by blockchain. Also, registration of equities will be mandatory and its privacy will be ensured, making stock manipulation by voting virtually impossible. The complex equation among brokers, regulators, and traders will be deleted - which, in turn, will give rise to a faster, cheaper, and less risky trade execution.

- Trade finance:

Trade finance participants need to keep a record of bills of trading, invoices, letters of credit etc. as transaction-related documents must be constantly reconciled against each other. With blockchain, all necessary information can be integrated into one digital document, with a clear date and time stamp, eliminating the need for several copies of the same document. These are updated in real-time and can be accessed by all network members, turning the procedure much less complicated.

- Digital identity verification and KYC:

Currently, online financial transactions involve a lot of steps, including personal verification, authentication, authorization etc.; that too for each new service provider. With blockchain, users can choose how they want to identify themselves and with whom they agree to share their identity, as well as register all this only once when they are provided with private and public keys - so KYC is done just once. This ledger can be used across banks to authenticate the identities of customers, saving everyone a ton of hassle.

- Financial inclusion:

People who want to avoid banks because of their high fees, asset requirements, regular income requirements, and minimum balance requirements to store money will immensely benefit from a blockchain ledger system. Their identities will be stored without the help of a central authority like a bank and they will be able to transact money simply with the help of a mobile device. By keeping costs low and allowing startups to compete against big banks, blockchain thus can promote financial inclusion.

- Investments:

The current investing model requires intermediaries such as investment bankers, venture capitalists, brokers, lawyers, etc. to create markets by matching investors with entrepreneurs, SMEs, and enterprises at every stage of growth from angels to IPOs. Blockchain’s decentralized peer-to-peer model allows pledges or individual investors to directly connect with creators and entrepreneurs to fund them. New projects can raise funds by releasing their own tokens that represent value and can later be exchanged for products, services, or cash. The whole process will be cheaper for both parties and much less complex.

Nevertheless, first, we need to solve a few primary issues with applying blockchain in finance

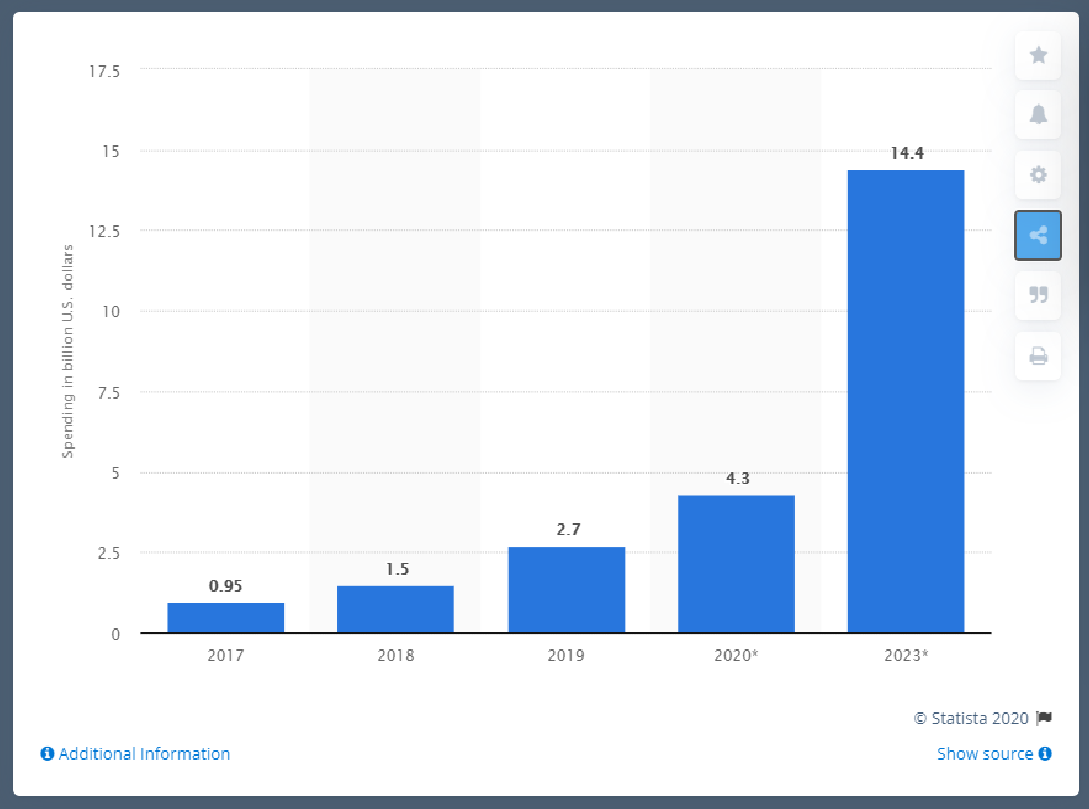

Blockchain in Australia arrived a long time ago and many financial organizations have already begun to accommodate this newcomer into their businesses. As a matter of fact, forecasts suggest that spending on blockchain solutions will continue to grow in the coming years, reaching over 14 billion U.S. dollars annually by 2023.

Even so, blockchain has not yet replaced the entire institution of finances. The reason behind this is not a lack of potential, but rather that the technology itself needs to evolve some more, as well as the world, needs to accept it more. Once we resolve the following issues, it won’t take long for this revolution to happen.

- Interoperability:

So far it seems like in order to use blockchain in finance, the existing systems need to be completely replaced, which is way too costly and not feasible at all. Blockchain will need to be compatible with different systems and should hold the potential to get adopted by the masses. Only then it can be used universally.

- Encryption:

A private key generated once has to be kept very securely as once it is misplaced or lost, there is no way to get it back. There needs to be a more secure system for recovering this encrypted key for the common people to use it as losing or forgetting a password is a very common occurrence.

What is more, even though once the data is stored in a blockchain ledger, it is immutable and resilient to hacking attacks, the data still can be stolen at the time of entering it to the ledger. This loophole needs to be eliminated first.

- Allowed permissions:

In order to make the blockchain ledger secure, there are layers of privacy applied on it. Almost every participant of the network will be given different levels of access permissions so that if one point is attacked by a hacker, the entire system doesn’t crumble. While it is a very effective method to use against hackers, it also makes the system overly complicated, which may not be so widely accepted.

- Scalability:

The network created through a blockchain should be able to handle the growing traffic while maintaining the speed of accessibility for the network participants, especially when it is applied to banking systems. Current blockchain has not been used on such a huge scale yet.

- Energy consumption:

Most of the current blockchain networks operate on the concept of proof-of-work mechanism where the members are rewarded based on how quickly they solve the equation to add a new block to the network. While this competition is good for the smooth-sailing of the procedure, it consumes a lot of energy, leaving a huge carbon footprint which will only be bigger if used on big institutions like banks. The rewards need to be more environmentally friendly before being used on such a large scale.

- Legal restrictions:

The essence of the current blockchain technology comes from its decentralized nature where it is not regulated by any central authority. However, this also makes the users vulnerable as they cannot seek help from the judiciary system at the instance of any crime. So if blockchain needs to be applied to institutions like banks, it needs to have some amount of government control to avoid chaos and to provide legal protection to the users.

Conclusion

Even though blockchain comes with its own risks and shortcomings, many major banks and stock exchanges in the world have already started to embrace the technology, and many big names in the finance industry like The American multinational investment bank and Goldman Sachs have invested heavily into the research for the same. Especially after the COVID-19 pandemic has exposed the sensitive nature of offline transactions, it is extremely likely that blockchain in Australia will be an integral part of finance very soon and the world will change forever.

About the Author:

Ralph Kalsi is an expert growth hacker that specializes in blockchain technology and digital marketing and the proud Sole Founder of Blockchain Australia Solutions.

Image source: Shutterstock